Bulk Chemicals

Titanium Dioxide (TiO2) Market Size, Share | Industry Report, 2024

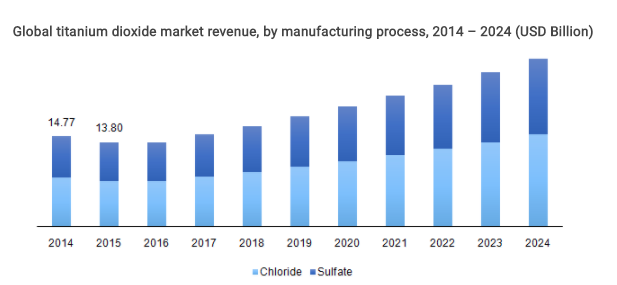

The global titanium dioxide market is expected to reach USD 27.49 billion by 2024 owing to the increasing demand of titanium dioxide in paper, paint & coating, cosmetics, and plastic industries. In 2014, DuPont Titanium Technologies started a manufacturing facility in Alamira, Mexico having a capacity of 200,000 tons/year which will help in fulfilling the demand worldwide.

Rising demand for lightweight automobiles is expected to play a vital role in the growth of global titanium dioxide market. Materials such as polycarbonates are used in the manufacturing of lightweight automotive which have low scratch resistance value. Also, the product is used in various industries such as chemical intermediates, fiber, technical titanium, inks for printer and rubber.

Access full report at https://www.hexaresearch.com/research-report/titanium-dioxide-industry

Keeping these driving factors in mind, companies are ramping up their production capacity. In 2015, PPG International entered into a partnership agreement with Henan Billions Chemicals Co. LTD. to set up a new manufacturing unit for titanium dioxide which is expected to produce 100,000 metric tons per year to expand its footprint in Asia Pacific. Companies such as Argex Titanium are using unique patented CTL process which involves low-cost feedstock material and solvent extraction method to produce a high-quality product.

Also, companies are focusing on increasing the applications of titanium dioxide int water treatment using techniques such as photocatalysis, in which titanium dioxide is used to speed up the solar disinfection process.

In 2016, paint & coating segment contributed 57.4% in terms of revenue. It was also extensively used in the plastics industry, paper industry, inks, and other specialty segments. The growth of these sectors is expected to boost the market positively over the next few years.

The plastic industry was the second largest segment due to the increasing applications as an excellent thermal stabilizer. In 2016 plastics segment contributed 23.2% in terms of revenue and is expected to grow with a positive CAGR during the forecast period.

Paper industry is the third largest user of titanium dioxide and contributed 10.4% in terms of revenue globally. Titanium dioxide is used in the manufacturing of decorative papers, these are used in the manufacturing of flooring, furniture, and wallpapers. Demand for high-end furniture is increasing which is expected to boost the demand for titanium dioxide. The paper industry is expected to contribute about 10.4% during the forecast period.

The global titanium dioxide market is expected to grow at a very lucrative rate due to its use in various above-mentioned industries. Also, titanium dioxide is used as a substitute for talc and kaolin which in turn is expected to boost the market for titanium dioxide.

Request for a free sample at https://www.hexaresearch.com/research-report/titanium-dioxide-industry/request-sample

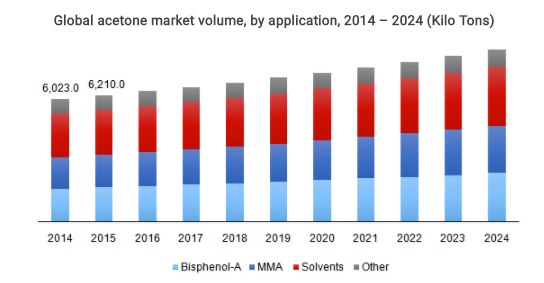

Global Acetone Market Size Expected To Reach $22.10 Billion By 2024 | Hexa Research

Bioplastics Market By Types, Application & Forecast 2024 | Hexa Research

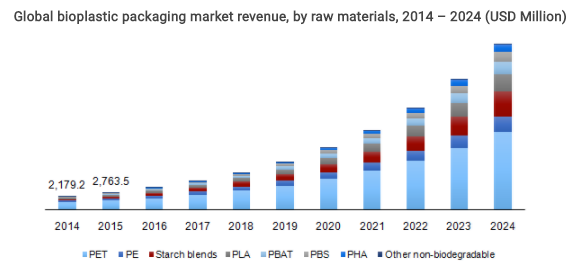

The global bioplastic packaging market to reach USD 34.24 billion by 2024, driven by the rising consumer demand for resource efficient and eco-friendly products. Europe was the largest market accounting for 32.7% of the volume share in 2016 due to supporting regulations coupled with consumer awareness regarding the conservation of the environment. North America and Asia-Pacific followed suit, where the regions together are expected to contribute USD 3.26 billion by 2024.

Keeping these driving factors in mind, companies are ramping up their production capacity as well as foraying into R&D of application of new biopolymers into mainstream applications. For instance, in October 2016, BASF and Avantium entered into a joint venture to form Synvina JV, which will manufacture and market FDCA and PEF. Synvina JV has a production capacity of 50,000 metric tons per year for FDCA and PEF.

Moreover, companies are focusing on R&D to expand the utilization of different raw materials such as PBS, PLA, and PBAT in various mainstream packaging applications. For instance, in April 2017, UK-based Biome Bioplastics developed a fully compostable and recyclable coffee cup made entirely from bioplastic materials. These factors together are expected to provide an impetus to the growth of the bioplastic packaging market over the next seven years.

PET dominated the global market contributing to USD 1.84 billion in 2016. The polymer was extensively used in rigid packaging on account of its high durability, transparency, and ease of moldability. Initiatives undertaken by companies such as Coca-Cola, P&G, and Heinz to use bio-based materials for packing beverages, sauces & spreads and cosmetics is expected to bolster the growth of the rigid packaging market.

Access full report or request for free sample at: https://www.hexaresearch.com/research-report/bioplastic-packaging-market

Increasing demand for flexible packaging solutions on account of several benefits including size and weight particularly in food applications coupled with rising demand for biodegradable films is anticipated to boost the growth of the market. The segment is expected to grow at a volume CAGR of 20.6% from 2017 to 2024.

Food packaging accounted for 9% of the overall market share in 2016 and is likely to witness above average growth as a result of rising consumer requirement for eco-friendly packaging. Aesthetic attributes such as transparency, size, weight, and presentation are expected to drive the growth of the segment over the projected period.

The growth of the global bioplastic packaging industry driven primarily by consumer demand is also likely to be favored by the implementation of stringent regulations for its synthetic counterparts. Despite the fall in crude oil prices, companies such as BASF, Arkema Dow, Solvay, and Braskem are continuing production at their facilities and focusing on R&D. These factors are likely to result in a tremendous growth of the global bioplastic packaging market growing at a revenue CAGR of 28.3% over the next seven years.

Aerospace Plastics Market To Grow At CAGR Above 10% Till 2024

The global aerospace plastics market stood nearly 57 kilotons in 2014. It is estimated to grow at over 10 percent CAGR from 2016 to 2024 (forecast period). Regulatory policies coupled with robust fiscal aid should be the key market propeller. The market will also be driven by usage in airplanes, alternatives for steel & aluminium, and expansion in the aviation industry.

The aviation industry is likely to observe high growth across Middle Eastern nations; like Qatar, U.A.E., and Saudi Arabia. Higher air traffic in defense & commercial sectors has contributed sales for the North American market. Strict policies on petrol-based products can hamper feed stock (high-grade plastics, etc.) availability.

For Market Research Report on “Aerospace Plastics Market” Visit – https://www.hexaresearch.com/research-report/aerospace-plastics-industry/

Moreover, adoption of carbon fibers in other applications may limit the availability of raw materials. Airplane manufacturers have begun employing a blend of thermoplastic & metal composites to lower fuel emissions and ensure passenger convenience. The aerospace plastics market is fragmented by applications, polymers, end-users, and geographies.

Applications comprise wings & rotor blades, air-frame & fuselage, and cabin areas. Air-frame & fuselage was the biggest segment in 2013. Demand for aerospace plastics in wings & rotor blades surpassed 7, 900 tons in 2014. ‘Plastics adoption’ in wings makes the latter quite resistant to metal fatigue. Demand for cabin area applications would grow at over 5 percent CAGR till 2024.

Polymers are polyether ketone ketone (PEKK), polyether ether ketone (PEEK), and polymethyl methacrylate (PMMA). PEKK was nearly USD 74.5 million in 2014. It has high ‘glass transition temperature’ & ‘mechanical load.’ PMMA generated around USD 168 million in 2014. It is used in flight decks & cockpits owing to its lightweight features.

Aerospace plastics do not rust and can function better than other materials. This characteristic bodes well for the aerospace plastics market and drives its incomes. End-users consist of military aircraft, general aviation, and commercial & freighter aircraft. Commercial & freighter was the biggest segment in 2013. Military aircraft are likely to experience the fastest growth.

Geographical regions encompass Europe, Asia Pacific, North America, and rest of the world. Europe dominated the global market in 2013. This region and Asia Pacific may be lucrative in the near future.

Oil Spill Management Market To Surpass $125 Billion By 2024

The global oil spill management market size is projected to grow beyond USD 125.62 billion by 2024. Growing incidents of oil spilling in the past along with severe safety and environmental policies are likely to propel the market over the forecast phase (2016-2024). Also, escalating pipeline and seaborne shipping of crude oil and chemicals could positively impact the market further.

The market is fragmented by technologies, techniques, applications, and regions. Technologies are Pre-oil spill and Post-oil spill. Pre-oil spill segment is divided into double-hull, pipeline, leak detection, blow-out preventers, and others. Double-hulling was the dominant segment in 2015 with highest shares.

For Market Research Report on “Oil Spill Management Market” Visit – https://www.hexaresearch.com/research-report/oil-spill-management-market

Marine trade registers for a majority of petroleum products and natural gas transportation. Mounting demand for crude and petroleum products oil in Europe and Asia Pacific will boost the maritime trade growth further. Post-oil spill segments are mechanical, chemical, biological, and physical. Chemical and mechanical containment and recovery are the techniques used in the industry.

By applications, the market can be sliced into pre-oil spill management a post-oil spill management. Pre-oil spill covers onshore and offshore sectors. The offshore segment recorded the maximum shares in 2015. It consumed approximately 70% of the total demand in that year.

Post-oil spill management also includes of onshore and offshore segments. In 2015, onshore post-oil spill sector was valued close to 60% of the total market demand. Regions such as Norway, U.S, Mexico, Canada, U.S., China, and Nigeria have observed well blowouts and occurrences of pipeline breakdowns. This could be accredited to huge market diffusion in past

Main regions in the market encompass North America, Europe, Asia-Pacific, the Middle East and Africa (MEA), and Central & South America. North America was the leading market for pre-oil spill management. It was estimated at 40.1% of total demand in 2015. This region will potentially face lucrative demand due to production activities and increasing oil & gas discovery. Pre-oil spill management shares in Asia Pacific will gain over USD 21,540 million by 2024. It is mounting at a healthy CAGR of 4.2% in the review phase.

Profits to determine hydrocarbon reserves noticeably and supportive government initiatives in the form of fiscal support in India and China could drive the regional demand. Top-most companies in the global oil spill management market include OMI Environmental Solutions, Skim Oil Inc., American Green Ventures Inc., and Spill Response Services.